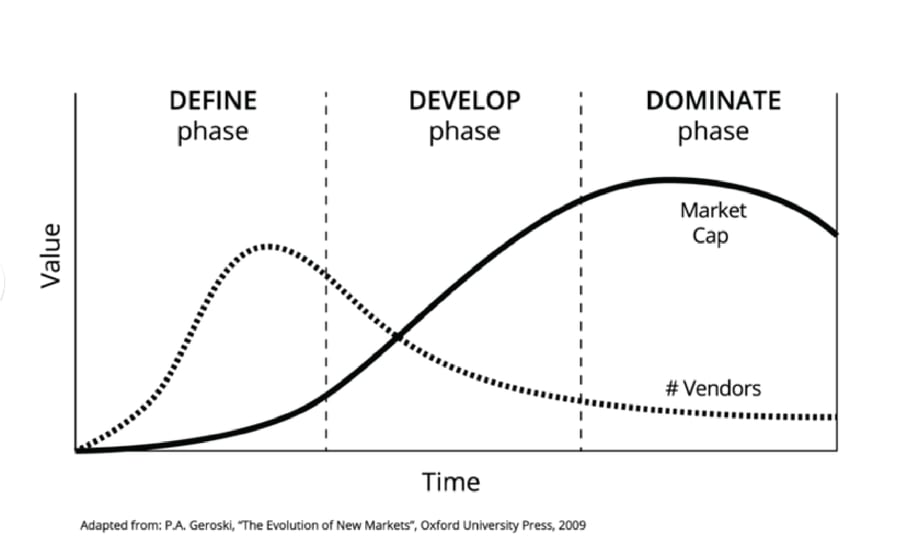

THE CATEGORY LIFECYCLE

Paul Geroski, author of The Evolution of New Markets, was an inspiration for some of our thinking. One of Geroski’s charts shows the stages in the evolution of a new market—that is, a new category. In a market’s earliest stage, the number of companies (he calls them providers) in the space, explodes. This is the phase when the new category is first defined and a gaggle of entrants are scrambling to solve the problem. In the middle phase, the number of companies dives as the king emerges and competitors disappear (because the king starts sucking up all the economics). In the last phase the number of companies bottoms out as the king dominates and reigns over the market. We adapted his work and created what we call the Category Lifecycle see Figure 1.

Figure 1: Category Lifecycle

EVOLUTION OF CATEGORIES OVER TIME

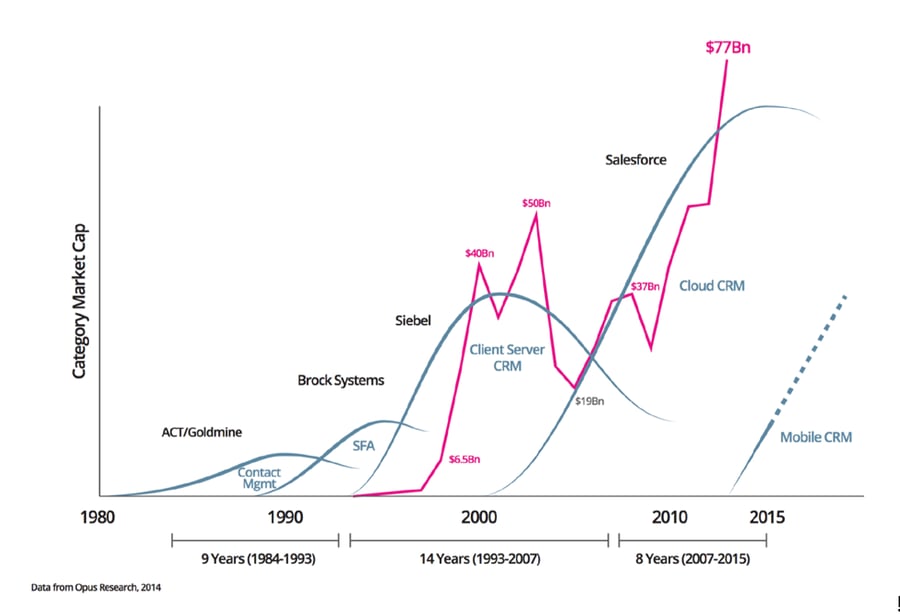

In our lectures and consulting work we often get asked the question of whether new categories emerge out of old categories and how do categories evolve over the long haul.

We contracted with Opus research to develop a timeline for the CRM category as a starting point for this discussion. See figure 2.

Figure 2: The Evolution of the CRM Category

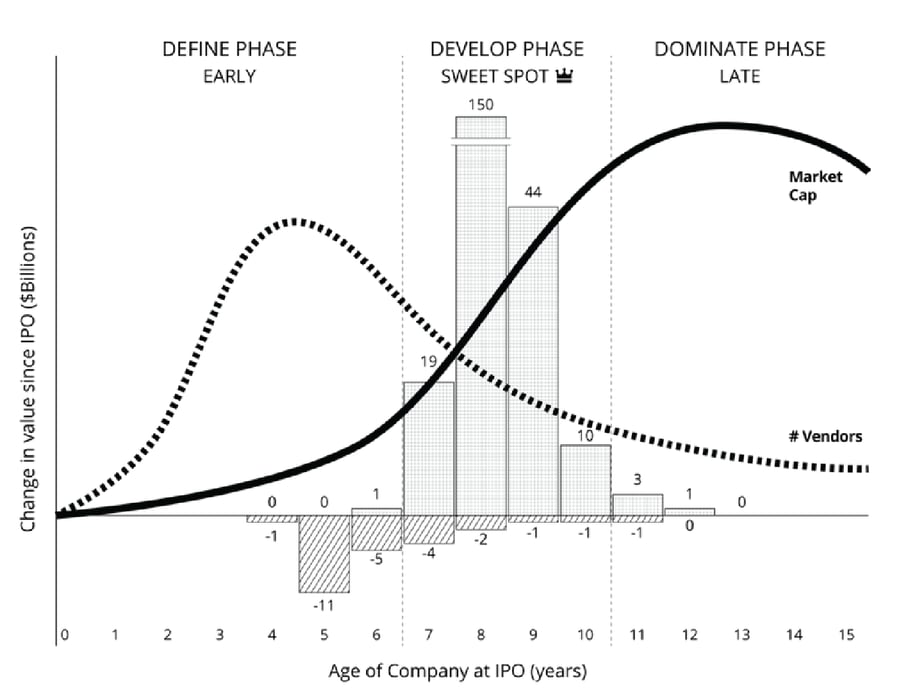

Value Creation and the 6-10 Law

Let’s go back to our 6-10 Law. This research showed us that companies that go public between the age of 6 and 10 years created more than 95% of the market cap for all technology companies founded since 2000.

We overlaid it on the Category Lifecycle and observed that the IPO sweet spot lands in the develop phase of the category lifecycle. See Figure 3. This seems to show that the best time for a category-creating company to go public (our data) and the moment of category explosion are the same.

And in the post-Internet era, that’s consistently been about six to ten years after the first companies are founded in the category. (Pre-Internet, categories took a little longer to spread throughout a market. In 1986, Microsoft went public in its sweet spot, and it was thirteen years old.)

Figure 3 // IPO Sweet Spot Overlay

Figure 3 // IPO Sweet Spot Overlay

We asked some of the leading investment bankers why the develop phase of the category lifecycle is so important. George Lee from Goldman Sacs was one of the first people we spoke with about this research. He said the develop phase of the category lifecycle curve is really interesting to public investors because two of the most important things these investors look for are growth and expanding margins. In the develop phase we see rapid adoption (revenue growth) and most vendors dropping away (increase in pricing power leading to expanding margins). So it makes complete sense that the category kings that go public during the develop phase of the category lifecycle share that value creation with the public markets and go on to dominate it.

While the principals of technology adoption have been explained well in books such as Crossing the Chasm or Gartner Hype Cycles, we wanted to explore more of the drivers of adoption and turned to some of the leading researchers in brain science. What we found was that changing perceptions of users and buyers are key to adoption and the reason the 6-10 law exists. Said another way, it often takes 6-10 years to change the minds of buyers and users.