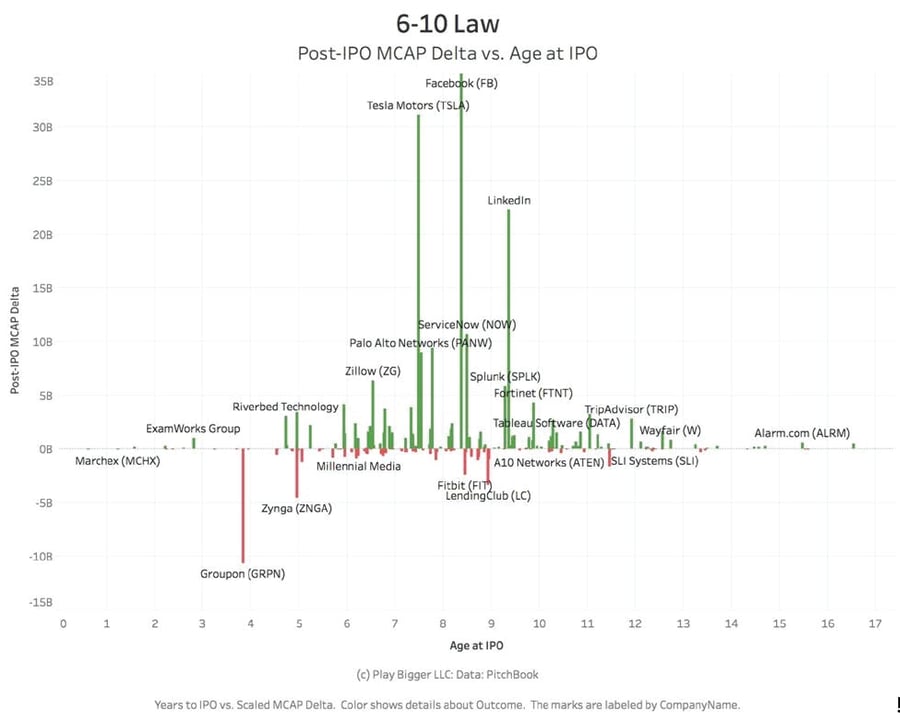

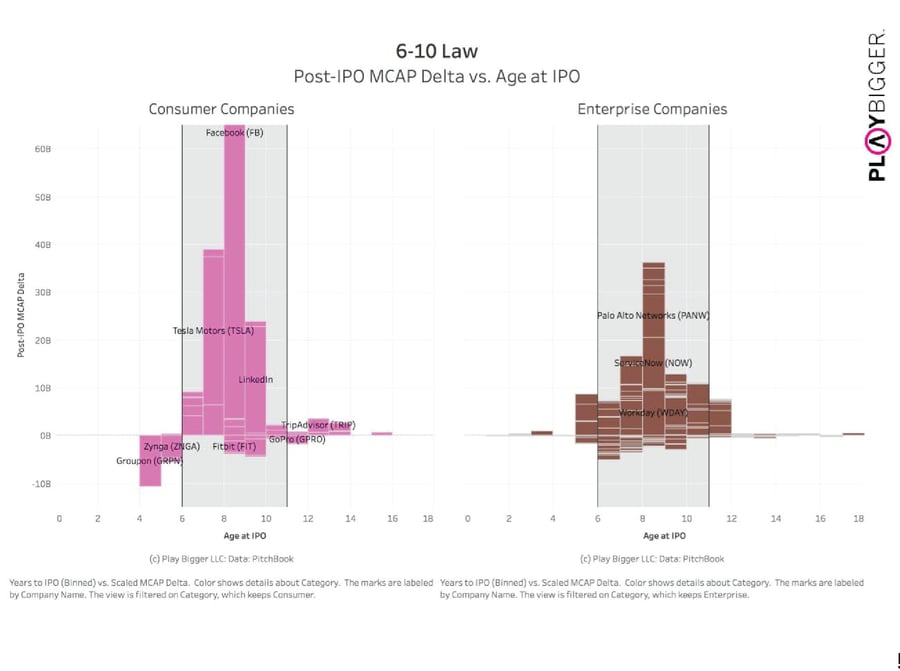

Figure 1 // 6-10 Law

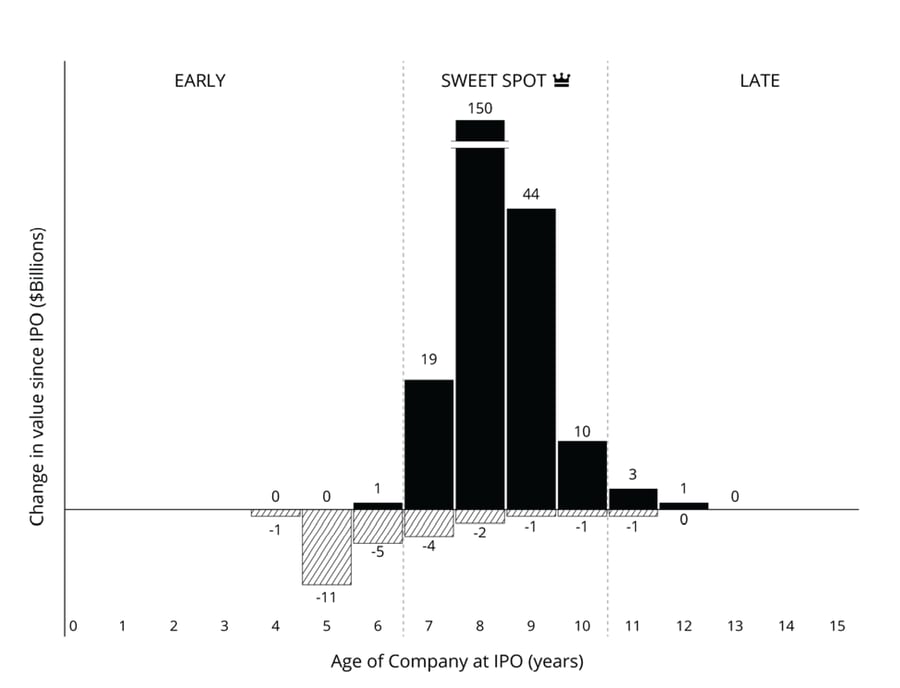

Figure 2 // IPO Sweet Spot Report

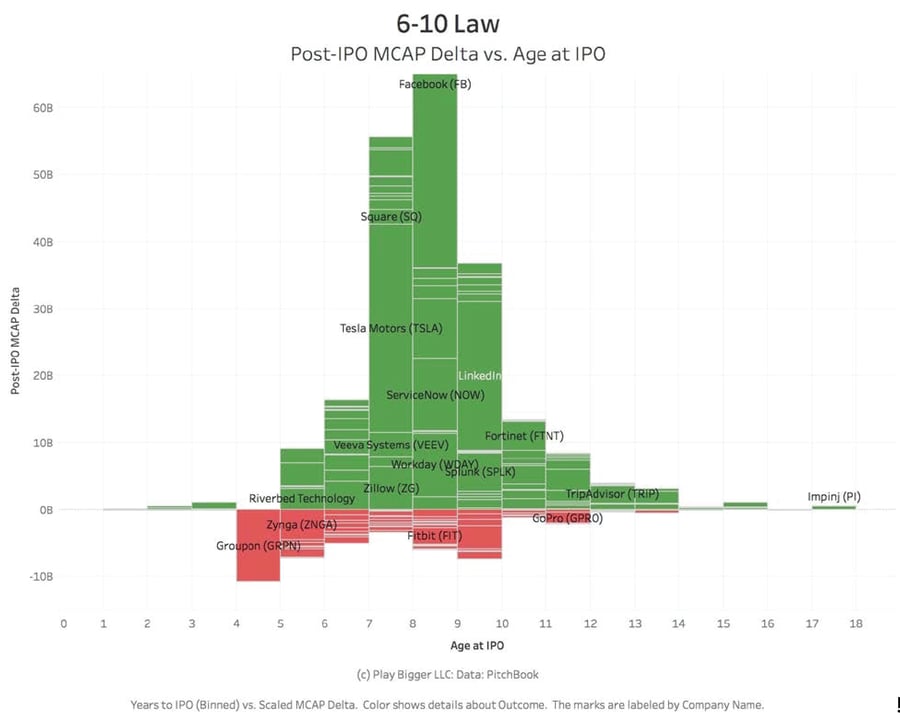

Figure 3 // 6-10 Law, 2017 Edition

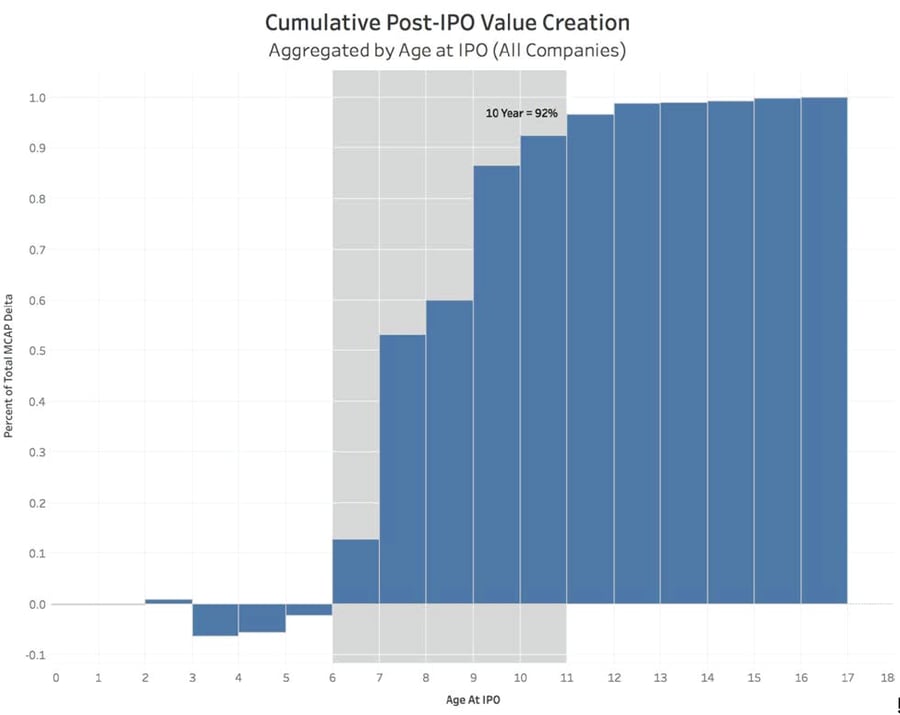

Figure 4 // Cumulative Value Creation Versus Age of Company at IPO

Figure 5 // Consumer Versus Enterprise

METHODOLOGY

Data Source and Selection

All Data utilized throughout this study was obtained from PitchBook, via extracts gathered by their support team.

We began by collecting data on companies that were VC-Backed, with headquarters in the United States, founded since 2000. Companies that were within PitchBook’s “Universe” of “Venture Capital” met this VC-Backed condition.

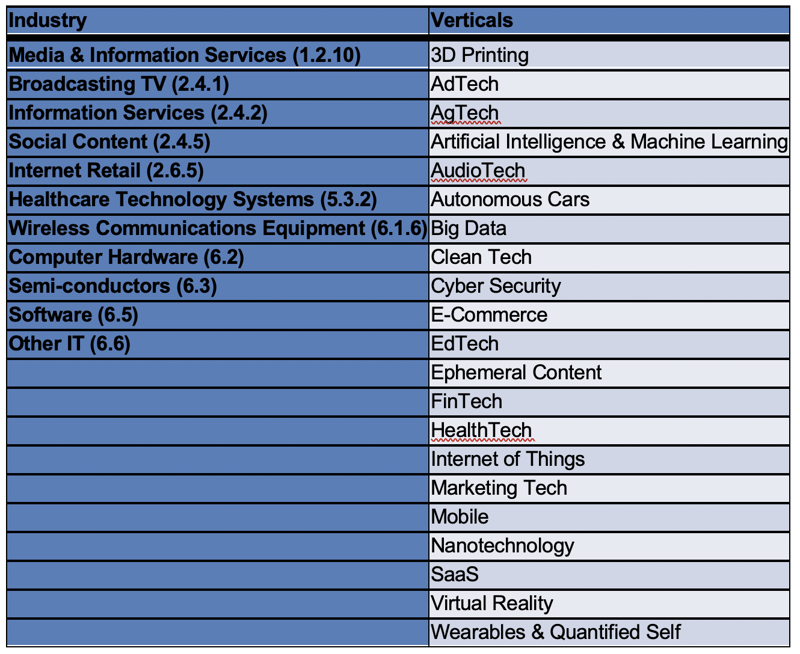

Companies were then only incorporated if they fell within our definition of a technology company, which meant that they needed to fall within at least one of PitchBook’s “Industry” or “Verticals” conditions. The conditions were selected through careful inspection of the companies, and iterative tuning of the conditions. Verticals included were intentionally kept broad.

Finally, companies were only kept if they made it to IPO.